Last-Minute US Tax Filing Tips for Freelancers

Table of Contents

The April deadline is days away, and if you’re a freelancer who hasn’t filed yet, you’re not alone. Millions of self-employed workers scramble every year to pull together their US tax filing tips for freelancers searches, 1099 forms, and deduction records before the clock runs out. The good news: last-minute doesn’t have to mean sloppy. With the right approach, you can still file accurately, claim what you’re owed, and avoid costly penalties.

Disclaimer: This article provides general information only and does not constitute tax advice. Consult a registered tax agent for advice specific to your circumstances.

Whether you’re a graphic designer, writer, consultant, or rideshare driver, this guide walks you through everything you need to do in the final stretch before the filing deadline.

Gather Your 1099-NEC Forms

Your first step is making sure you have all your income documented. Every client who paid you $600 or more during the tax year should have sent you a Form 1099-NEC. Check your email, your physical mailbox, and any freelance platforms you used – many platforms like Upwork, Fiverr, and Stripe issue 1099s electronically.

Here’s the critical point: even if you didn’t receive a 1099 from a client, you’re still required to report that income. The IRS expects you to declare all self-employment income, regardless of whether the payer issued a form. Cross-reference your bank statements and invoicing records against the 1099s you received to catch any gaps.

If a 1099 contains errors – wrong amount, wrong Social Security number – contact the client immediately and request a corrected form. Filing with incorrect information can trigger IRS notices down the road.

Last-Minute US Tax Filing Deductions to Check

When you’re rushing to file, deductions are where money gets left on the table. Take 30 minutes to review these commonly overlooked categories before you submit:

- Home office – If you used part of your home regularly and exclusively for business, you can claim either the simplified method ($5 per square foot, up to 300 sq ft) or the actual expense method. Even if you didn’t track actual expenses, the simplified method requires no receipts beyond proof you had a dedicated workspace.

- Vehicle mileage – If you drove for business at all – client meetings, supply runs, site visits – you can deduct either the IRS standard mileage rate or actual vehicle expenses. Check your calendar and Google Maps timeline to reconstruct trips you may have forgotten.

- Health insurance premiums – Self-employed individuals can deduct 100% of premiums paid for health, dental, and vision coverage for themselves and their families, provided they weren’t eligible for an employer-sponsored plan.

- Software and subscriptions – Adobe Creative Cloud, Slack, Zoom, QuickBooks, cloud storage, project management tools – anything you paid for that’s directly related to your freelance work is deductible.

- Professional development – Online courses, conferences, books, certifications, and coaching sessions related to your field.

- Retirement contributions – Contributions to a SEP-IRA can be made up until the filing deadline (including extensions), so you can still make a last-minute contribution to reduce your taxable income.

- Phone and internet – The business-use percentage of your cell phone bill and home internet is deductible.

For a deeper dive into tracking these expenses year-round, see our guide to 1099 expense tracking.

Catch Up on Estimated Tax Payments

Freelancers are generally required to make quarterly estimated tax payments throughout the year using Form 1040-ES. If you missed one or more payments, you’ll likely owe an underpayment penalty – but filing now and paying what you owe minimizes the damage.

The IRS charges a penalty on the amount of estimated tax you should have paid but didn’t, calculated from the due date of each quarterly installment. The penalty rate is tied to the federal short-term interest rate and adjusts quarterly.

If your income was uneven throughout the year – say you earned most of it in Q4 – you may be able to reduce your penalty by filing Form 2210 and using the annualized income installment method. This shows the IRS that you couldn’t have known earlier in the year how much you’d owe.

The bottom line: even if you can’t pay the full amount right now, file your return on time and pay as much as you can. The failure-to-file penalty is much steeper than the failure-to-pay penalty.

Filing an Extension with Form 4868

If you simply can’t get everything together by the deadline, file Form 4868 for an automatic six-month extension. This gives you until October 15 to submit your return.

A few important things to understand about extensions:

- An extension to file is not an extension to pay. You still need to estimate what you owe and send payment by the original April deadline. If you underpay, interest and penalties accrue on the unpaid balance.

- Filing the extension is free and easy. You can do it electronically through IRS Free File, most tax software, or by mailing the paper form.

- There’s no penalty for filing an extension. The IRS grants them automatically – you don’t need to provide a reason.

An extension is always better than not filing at all. The failure-to-file penalty starts at 5% of unpaid taxes per month, up to a maximum of 25%. The failure-to-pay penalty is only 0.5% per month. The math heavily favors filing something on time.

Common Last-Minute Mistakes to Avoid

When you’re filing under pressure, errors are more likely. Watch out for these:

- Missing income – Forgetting a side gig, a small client, or platform payouts. Cross-check every income source.

- Incorrect Social Security number – A single wrong digit can delay processing and trigger notices.

- Not signing your return – Unsigned returns are treated as not filed. If filing jointly, both spouses must sign.

- Wrong bank account numbers – If you’re expecting a refund via direct deposit, double-check the routing and account numbers. A mistake here can delay your refund by weeks or months.

- Forgetting state taxes – Many states have their own filing requirements and deadlines. Don’t assume federal filing covers everything.

- Claiming the wrong filing status – If your personal situation changed during the year (marriage, divorce, new dependent), make sure your filing status reflects your situation as of December 31.

How Taxr Helps You Avoid the Last-Minute Rush

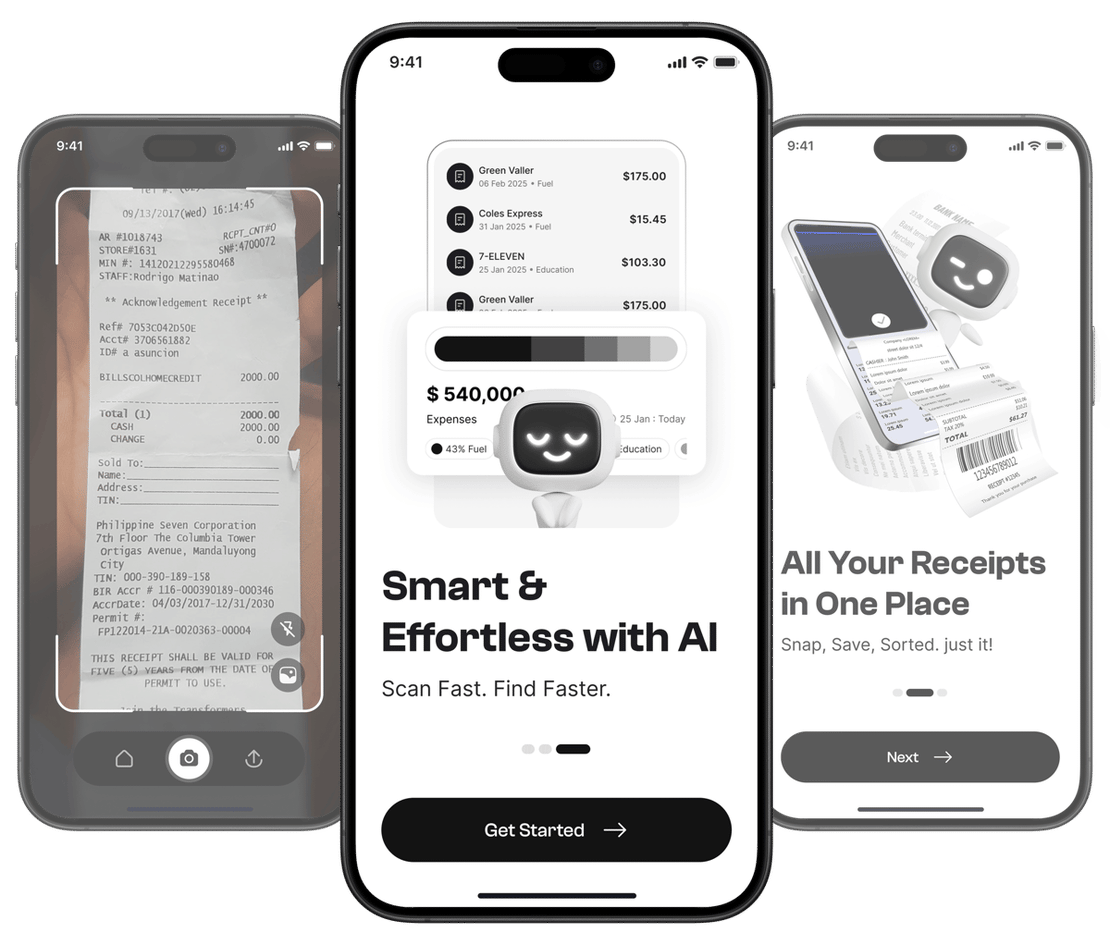

The best last-minute tip is not to be in this position next year. Taxr makes year-round expense tracking effortless for freelancers – snap a photo of any receipt and the AI instantly extracts the date, amount, vendor, and category. Every expense is stored securely, organized, and ready to export when tax season arrives.

Instead of scrambling through a year’s worth of bank statements and email receipts, you’ll have a clean, categorized record of every deductible expense at your fingertips. You can export your data by category, filter by date range, and export what you need as an Excel or PDF report.

Stop dreading April. Start tracking now and make next year’s filing deadline feel like just another day.